Market Research

The State of Indian Manufacturing Market Research Report

1. Industry Overview & Executive Summary

If you zoom out and look at India’s manufacturing story right now, it feels less like a straight line and more like a build phase. New capacity is coming online. Global buyers are testing India as a serious alternative in their supply chains. Policy is pushing hard. And yet, inside factories, the real work is still about yield, uptime, and getting shipments out on time. This section lays out the size of the sector, its growth trajectory, what’s driving it, and how finance, marketing, and operations are evolving together.Industry size and growth

Manufacturing is a central pillar of India’s growth strategy, and the numbers show momentum.- Manufacturing Gross Value Added (GVA) reached ₹24.6 lakh crore in FY24, up 11.9 percent year-on-year. (Economic Times)

- India’s manufacturing PMI has remained firmly in expansion territory (above 50) through mid-2024, with readings in the high 50s, signaling broad-based growth in output and new orders. (Moneycontrol)

- MSMEs account for roughly 35.4 percent of manufacturing output and around 48.6 percent of exports, underscoring how deeply the sector relies on small and mid-sized firms. (Economic Times)

Macro outlook

Three forces are shaping the near-term macro trajectory:- Policy-backed industrialization The Production-Linked Incentive (PLI) schemes across 14 sectors have reportedly generated ₹1.61 lakh crore in actual investment, ₹14 lakh crore in production/sales, and over 11.5 lakh jobs (direct and indirect) through November 2024. (PIB)

- Global supply chain realignment Large global buyers are diversifying beyond single-country sourcing models. India is increasingly positioned as a complementary manufacturing hub, particularly in electronics, auto components, defense, and chemicals.

- Infrastructure and logistics reform India recently published a detailed logistics cost assessment estimating total logistics costs at 7.97 percent of GDP in 2023–24. That level of transparency is important. It means cost competitiveness is now being measured, not guessed. (DPIIT)

Key drivers of industry growth

Here are the structural drivers you can’t ignore: Capacity build-out in priority sectors Electronics manufacturing services (EMS), specialty chemicals, auto components, and defense manufacturing are all seeing capital formation. Acquisitions in EMS and precision manufacturing show companies are buying capability, not just land. (Tata Electronics) Export orientation MSMEs and large firms alike are increasingly export-facing. With nearly half of exports tied to MSMEs, the export engine is widely distributed, not concentrated in a few giants. Digitization across the value chain From ERP adoption to digital procurement and AI-enabled quality inspection, technology is creeping into core manufacturing processes. This shift is less flashy than consumer tech, but operationally transformative.Cross-functional summary: finance, marketing, operations

Finance

Capital allocation is shifting toward: • Vertical integration and platform consolidation • Capacity expansion in PLI-supported sectors • Capability acquisitions in precision manufacturing and EMS FDI equity inflows into manufacturing increased from $98 billion (2004–2014) to $165 billion (2014–2024), reflecting sustained foreign interest. (PIB) The financial story is not just growth. It’s strategic concentration. Companies are building defensible positions through scale, certifications, and supply chain depth.Marketing

Manufacturing marketing used to be relationship-first, almost invisible. Now it’s hybrid. Buyers conduct digital due diligence before first contact. They expect: • Clear capability pages • Certifications and compliance documentation • Fast, accurate RFQ turnaround • Evidence of export experience Industrial branding is shifting from “we are trusted” to “here is proof.” The companies that win RFQs consistently are often those that respond fastest with the cleanest documentation.Operations

Operationally, three themes dominate:- Logistics optimization With logistics cost now quantified at 7.97 percent of GDP, firms are analyzing lane-level costs, port charges, and mode mix with more discipline. Source: (DPIIT)

- Quality systems and traceability Export-driven growth requires audit-ready operations. Certification, inspection systems, and process documentation are becoming competitive differentiators.

- Workforce skill depth Growth is constrained less by headcount and more by supervisory capability, maintenance skill for automated systems, and quality engineering.

Industry Snapshot Table

| Dimension | Latest Snapshot | Strategic Meaning |

|---|---|---|

| Manufacturing GVA (FY24) | ₹24.6 lakh crore | Strong value-add base, formal sector momentum |

| Growth (FY24 YoY) | +11.9% | Output expansion across segments |

| Logistics cost (FY24) | 7.97% of GDP | Competitiveness hinge point |

| PLI reported investment (through Nov 2024) | ₹1.61 lakh crore | Policy-backed industrial scaling in priority sectors |

| MSME share of manufacturing output | ~35.4% | Supply chain depth (and fragmentation) sits here |

Global Hubs and Growth Geographies Map

2. Finance & Investment Landscape

Money is flowing into Indian manufacturing. But it’s not random. It’s selective, strategic, and increasingly tied to capability rather than just capacity. If Section 1 described the momentum, this section explains where capital is concentrating, how deals are structured, and what healthy (or fragile) unit economics look like across subsectors. Let’s unpack it properly.Recent M&A Activity

Manufacturing M&A in India over the past 12–18 months reflects three recurring motives:- Platform building in electronics and precision manufacturing

- Brand and distribution capture in consumer-facing manufacturing (e.g., paints, materials)

- Capability acquisition in defense, aerospace, and high-compliance sectors

Deal Table

| Buyer | Target | Segment | Deal Value | Date Announced | Strategic Rationale | Source |

|---|---|---|---|---|---|---|

| JSW Paints | AkzoNobel India (stake up to 74.76%) | Paints & Coatings Manufacturing | ₹8,986 crore | June 2025 | Brand expansion, distribution scale, manufacturing footprint consolidation | Business Standard |

| Tata Electronics | Pegatron Technology India (60% controlling stake) | Electronics Manufacturing Services (EMS) | Undisclosed | January 2025 | Platform consolidation in device manufacturing and supply chain integration | Tata Electronics Press Release |

| Tube Investments of India | Orange Koi (87% staged acquisition) | Precision Manufacturing (Metal Injection Molding) | Up to ₹73 crore | January 2026 | Acquisition of advanced process capability in high-precision components | Times of India |

| Sigma Advanced Systems | AS Strategic | Aerospace & Defense Manufacturing | ₹30 crore | January 2026 | Expansion of global aerospace and defense platform capabilities | Economic Times |

- Capability > capacity Acquirers are buying certification history, customer relationships, and technical know-how.

- Electronics is a focal point EMS and component-level integration continue to draw capital due to export potential and policy tailwinds.

- Defense and aerospace are strategic Not volume-driven yet, but high-margin and sticky once qualified.

Investment Trends

Policy-Driven Capital Production-Linked Incentive (PLI) schemes have reportedly generated:- ₹1.61 lakh crore in actual investment • ₹14 lakh crore in cumulative production/sales • 11.5+ lakh jobs

- Industrial automation • Specialty chemicals • Contract manufacturing • Defense components

Revenue Models & Unit Economics

Indian manufacturing is not monolithic. Unit economics differ dramatically by model. Let’s break it down clearly.- Asset-Heavy Commodities (Steel, Cement, Base Chemicals)

- Precision Components & High-Compliance Manufacturing

- Moderate gross margins • High customer retention • Longer sales cycles • Lower marketing spend but higher documentation cost

- Electronics Manufacturing Services (EMS)

- Sales engineering cost • Travel + technical pre-sales • Sampling/prototyping • Compliance audits

- Repeat orders • Tooling revenue • Service contracts • Spare parts

LTV:CAC Ratio Chart

| Segment | Typical CAC Intensity | LTV Characteristics | Illustrative LTV:CAC Ratio | Strategic Interpretation |

|---|---|---|---|---|

| Commodity Manufacturing | Low | Volume-driven repeat business, price sensitive | 3.0x | Stable but margin-sensitive; depends heavily on scale and cost efficiency |

| Precision / Aerospace Manufacturing | High | Long qualification cycles, multi-year contracts | 5.5x | High lifetime value once approved; strong stickiness and switching costs |

| Electronics Manufacturing Services (EMS) | Medium | Contract-based repeat orders, renegotiation risk | 3.8x | Moderate economics; scale and yield efficiency drive profitability |

Financial Health Indicators

What investors and lenders watch in Indian manufacturing:- Working Capital Cycle Days inventory + days receivable – days payable This often determines survival during slowdowns.

- Capacity Utilization Below 70 percent utilization often pressures margins significantly.

- EBITDA Stability Cyclical sectors see volatility; diversified product mix smooths this.

- Debt to EBITDA High capex sectors carry leverage risk. Interest rate shifts matter materially.

- Export Mix Firms with diversified export exposure are less vulnerable to domestic demand shocks.

EV/Revenue + EV/EBITDA Multiples

| Subsector | EV / Revenue (x) | EV / EBITDA (x) | What Drives the Multiple |

|---|---|---|---|

| Steel & Base Metals | 0.8x – 1.8x | 5x – 9x | Cyclicality, commodity pricing, capacity utilization |

| Cement | 2.0x – 4.0x | 10x – 18x | Regional dominance, demand visibility, pricing power |

| Specialty Chemicals | 2.5x – 6.0x | 12x – 25x | Export exposure, customer stickiness, product complexity |

| Auto Components | 1.5x – 3.5x | 8x – 16x | OEM diversification, EV exposure, margin stability |

| Electronics Manufacturing Services (EMS) | 1.0x – 3.0x | 10x – 20x | Growth visibility, scale, global customer base |

| Aerospace & Defense Manufacturing | 2.5x – 6.0x | 15x – 30x | Long-term contracts, high compliance barriers |

| Industrial Automation & Capital Goods | 1.5x – 4.0x | 12x – 22x | Order backlog visibility, export mix, tech integration |

3. Marketing Performance & Trends

Manufacturing marketing in India has quietly changed jobs. It used to be: find a few buyers, fly out, shake hands, get qualified, repeat. Now it’s: buyers shortlist you online, compare you against alternatives, build internal consensus, then contact you when they’re already deep into the decision. That shift changes what works, how you measure ROI, and what “good marketing” even means.Channel breakdown: SEO, paid, influencer, email, events

The big idea: in manufacturing, marketing ROI is less about “traffic” and more about reducing buyer risk. If your marketing makes procurement feel safer choosing you, you win. A useful reality check: • Many B2B buyers prefer to research independently, and irrelevant outreach can actively hurt. Gartner reported 61% of B2B buyers prefer a rep-free buying experience and 73% avoid suppliers who send irrelevant outreach. (Gartner) • Separate research from outreach: the anonymous research phase is now where preferences form. A 6sense Buyer Experience report summary (via Demand Gen Report) notes buyers are often far into their journey before they engage sellers, and many have a preferred vendor at first contact. (Demand Gen Report)Multi-Channel Performance Table

| Channel | Best for | Typical ROI signal to track | Common pitfall | Practical move that improves results |

|---|---|---|---|---|

| SEO and technical content | Export discovery, inbound RFQs, credibility | RFQs per month, RFQ-to-quote rate, quote-to-order rate | Writing generic content that attracts low-intent traffic (students, competitors) | Build capability pages by part family (materials, tolerances, standards, industries, lead times) |

| Paid search | High-intent terms (specific processes, materials, part types) | Cost per qualified RFQ, win rate by keyword cluster | Paying for broad keywords like “manufacturer in India” | Bid on spec-level intent and gate with RFQ forms that collect the right fields |

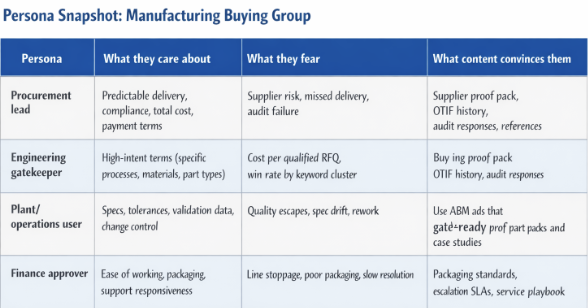

| LinkedIn paid and ABM | Targeting procurement and engineering personas at named accounts | Meetings booked, account engagement, influenced pipeline | Running “brand ads” with no proof or differentiation | Use ABM ads that point to audit-ready proof packs and case studies |

| Email (nurture) | Distributor networks, repeat orders, spares, reactivation | Reply rate, quote requests, reorder rate | One-size-fits-all newsletters | Segment by industry, plant type, and buyer stage (procurement vs engineering vs owner) |

| Events and trade shows | High-ticket categories, partnerships, exports | Pre-booked meetings, post-show RFQs, conversion speed | Treating events as “visibility” instead of a pipeline machine | Lock meetings before the event and run a strict 7/14/30-day follow-up cadence |

| Short-form video and social | Employer brand, MSME visibility, product storytelling | Inbound inquiries, distributor interest, hiring conversion | Making it entertainment-only | Keep it proof-led: shop-floor clips, inspection process, packaging, dispatch discipline |

Buyer behavior trends: what’s changing, what triggers decisions

The modern manufacturing buyer is more cautious, more documented, and less patient. What’s driving that:- Research-first buying Buyers want to do their own homework before talking to sales. Gartner’s data reinforces a strong preference for independent digital research. (Gartner)

- Anti-spam instincts Irrelevant outreach creates distrust. That 73% “actively avoid” statistic is brutal, but it matches what many sales teams feel in practice: sloppy targeting is expensive and reputation-damaging. (Gartner)

- Traceability and “show me” expectations In export-linked supply chains, traceability and tamper-proof documentation are becoming part of brand trust, not just compliance. PwC’s work on traceability frames how trust is rebuilt through verifiable supply chain records. (PwC)

Persona Snapshot

Creative and messaging that performs best

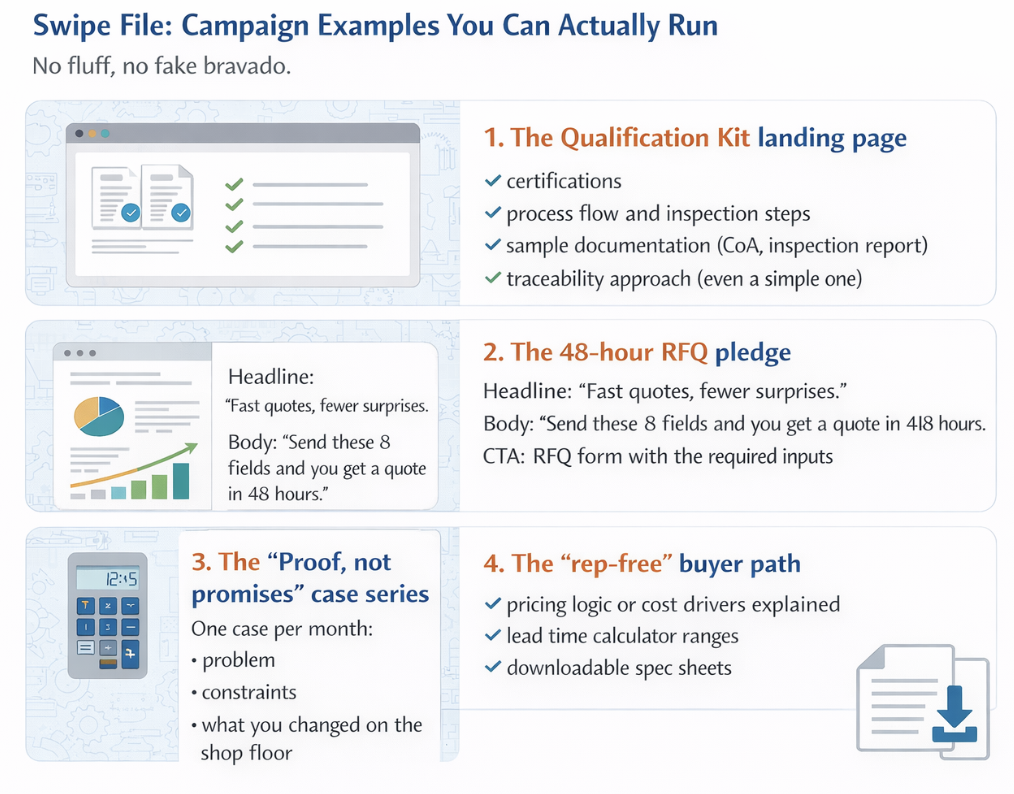

What works best right now is not “we are world-class.” It’s “here’s proof, and here’s how we run.” High-performing messaging patterns- Capability clarity Spell out what you can do with specifics: materials, machines, tolerances, standards, testing, lead time bands, MOQ logic.

- Risk reduction Procurement teams buy safety. Give them: • Certifications and audit summaries • Traceability approach • Packaging and dispatch discipline • Corrective action process

- Speed and certainty A strong promise is: “You’ll have a quote in 48 hours if you provide these inputs.” Then you publish the input checklist and stick to it.

Market positioning and brand perception

In Indian manufacturing, brand is less about vibes and more about confidence. Most buyers mentally score you on: • Compliance credibility (certs, audits, documentation discipline) • Delivery reliability (lead time honesty, packaging, OTIF consistency) • Responsiveness (how fast you quote, how fast you fix) • Transparency (clear limits, clear escalation paths) A strong positioning line in this market is usually some version of: “We are the supplier you can sleep on.” Not glamorous, but it sells.Swipe File: Campaign Examples

4. Operational Benchmarking

If finance is the fuel and marketing fills the pipeline, operations is where manufacturing wins or loses. Quietly. Repeatedly. Every shift. India’s manufacturing growth story now depends less on ambition and more on execution discipline: logistics efficiency, workforce capability, tech adoption, and compliance rigor. This section breaks down the operational realities that separate average plants from export-ready leaders.Supply Chain & Logistics

Logistics is no longer a black box. India’s official logistics cost assessment estimates total logistics cost at 7.97% of GDP in 2023–24 (₹24.01 lakh crore). (DPIIT) That figure matters because:- Even a 1% improvement materially improves export competitiveness • Freight mode mix (road vs rail vs coastal shipping) directly impacts margin • Port-related charges and documentation inefficiencies compound cost leakage

Workforce Structure

India’s manufacturing employment expanded alongside FY24 growth. But headcount isn’t the main issue. The constraint is skill density. Critical skill gaps frequently appear in:- Automation maintenance (PLC, robotics troubleshooting) • Quality engineering and statistical process control • Supervisory shift leadership • Documentation and audit readiness

- Increasing automation in electronics and precision manufacturing • Greater demand for diploma-level technical staff • Hybrid model: core in-house + contract labor flexibility • Rising wage competition in manufacturing hubs

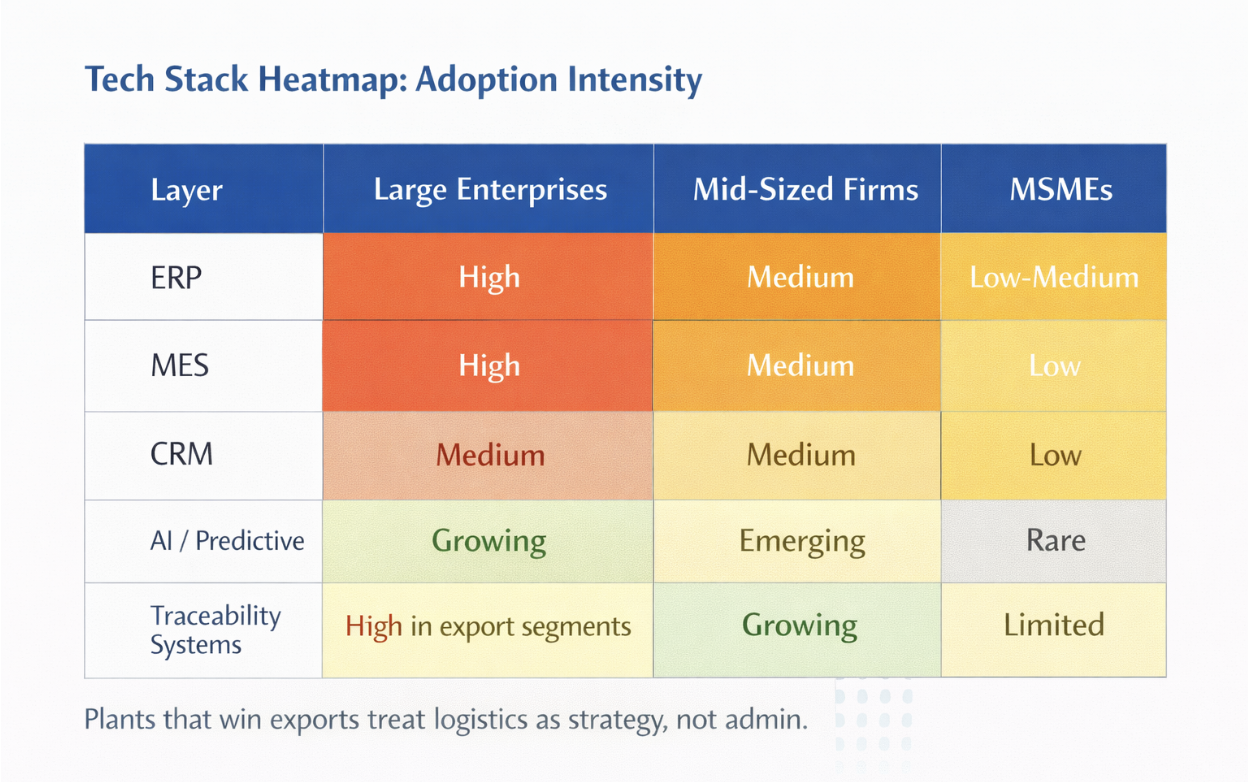

Technology Stack

The manufacturing tech stack is no longer optional. It’s layered. Core Layer (System of Record) • ERP systems (SAP, Oracle, Microsoft Dynamics, Ramco, Tally for SMBs) • Financial + inventory integration • Order tracking Execution Layer • MES (Manufacturing Execution Systems) • SCADA / PLC integrations • Shop-floor data capture • Quality inspection systems Commercial Layer • CRM (Zoho, Salesforce, HubSpot common in mid-size firms) • CPQ or structured quoting workflows • RFQ tracking dashboards Emerging Layer • AI-driven predictive maintenance • Vision-based inspection systems • Digital twin simulations in advanced plants • Traceability solutions for export compliance Operational Insight: Most performance gains now come not from installing tech, but from integrating it properly. ERP without disciplined data entry creates reporting illusions. MES without supervisor buy-in creates shadow spreadsheets.Fulfillment & Customer Service Strategy

Customer service in manufacturing is operational. It includes: • Escalation matrix • Replacement timelines • Packaging discipline • Clear SLA definitions • Corrective action transparency Best-in-class manufacturers:- Publish packaging standards • Define response SLAs (e.g., 24-hour root cause acknowledgment) • Maintain structured CAPA documentation • Track repeat defect patterns

Regulatory & Compliance Environment

Compliance burden varies by subsector, but commonly includes:- Environmental clearances • Labor law compliance • Product testing and certification • Export documentation requirements • Sector-specific certifications (defense, aerospace, pharma, etc.)

Tech Stack Heatmap

Ops KPI Table

| KPI | Why it matters | Benchmark discipline |

|---|---|---|

| OTIF (On-Time In-Full) | Direct driver of renewal, buyer trust, and escalation frequency | Track by customer tier and lane (domestic vs export); trend weekly and monthly |

| Inventory Days (RM / WIP / FG) | Working capital lock-up; impacts cash cycle and resilience during demand swings | Track separately by category and product family; set thresholds by lead-time volatility |

| Freight Cost (% of Sales) | Margin protection; reveals lane-level cost leakage and mode-mix issues | Break down by domestic vs export and by lane; review mode mix quarterly |

| Quote-to-Dispatch Lead Time | Buyer experience signal; influences win rate and repeat orders | Track by SKU family and customer tier; separate standard vs engineered-to-order |

| Export Documentation Cycle Time | Prevents demurrage and missed vessel cutoffs; reduces last-minute firefighting | Use a standardized checklist; audit exceptions and rework causes monthly |

5. Competitor & Market Landscape

Indian manufacturing is not one market. It’s a quilt: cement consolidates like an oligopoly, passenger vehicles behave like a high-speed consumer market with brutal share fights, electronics manufacturing is scaling fast under policy support, and steel stays cyclical but capacity-led. That mosaic matters because “top competitors” depends on what you’re buying: a ton of cement, a stamped bracket, a phone sub-assembly, or a defense-grade subsystem. So this section maps the landscape in the way procurement teams actually see it: by subsector and by buyer risk.Top players and market structure (by subsector)

- Autos (retail-led, share math is visible) Passenger vehicles: Maruti Suzuki remains the anchor at 40.25% FY’25 retail market share, with Hyundai (13.46%), Tata Motors (12.90%), and Mahindra (12.34%) forming the next tier. (fada.in)

- Brand and distribution are moats in PV.

- For CV, uptime economics and fleet relationships matter more than glossy brand.

- Cement (consolidation, scale wins) ICRA expects the top five cement companies’ market share to rise to 55% by March 2025, reflecting ongoing consolidation. (ICRA, NDTV Profit)

- The big players compete on logistics reach, captive power/fuels, and limestone security.

- M&A is a recurring play because buying capacity is often faster than building it (ICRA’s consolidation framing is the tell). (NDTV Profit, Business Standard)

- Steel (scale, cycles, and utilization discipline) India’s Ministry of Steel annual report notes crude steel production rose from 109.137 MT (2019–20) to 144.299 MT (2023–24), and highlights India as the world’s 2nd largest crude steel producer (calendar year 2023, provisional). (steel.gov.in)

- Large integrated players win on cost, captive raw materials, and downstream value-added mix.

- Mid-size players win by specializing (coated, tubes, engineered products) and staying nimble in regional markets.

- Electronics manufacturing (fast-scaling ecosystem, still sorting winners) The EMS category is in expansion mode, with leading listed players like Dixon building new capacity and moving into IT hardware and industrial electronics, including partnerships aimed at PCs/servers and broader industrial products. (The Times of India)

- The moat is execution: yields, QA, and customer concentration management.

- The next moat is component depth (moving beyond assembly).

- Manufacturing platforms and automation (new kind of competitor) Two “meta-competitors” are changing how capacity is bought and deployed:

- Aggregating capacity (platforms) so buyers can source faster

- Reducing labor dependence (automation) so plants can scale with fewer bottlenecks

Emerging startups or disruptors to watch (practical, not hype)

Here’s a short list of “watch because it changes buyer behavior” names and categories, with what they disrupt:- Capacity aggregation / sourcing Zetwerk: compresses sourcing cycles for buyers who want diversified supplier options with one interface. (zetwerk.com, The Financial Express)

- Industrial robotics and warehouse automation Addverb: pushes automation into operations where India is still under-automated, which matters for cost, safety, and throughput. (The Economic Times)

- Localization-led electronics manufacturing Dixon’s facility expansion and product diversification signals a shift toward broader electronics categories and deeper capability. (The Times of India)

Competitive Matrix (Product vs. Reach vs. Pricing)

| Cluster | Typical players | Product (offer) | Reach (go-to-market footprint) | Pricing posture | How they win | How they lose |

|---|---|---|---|---|---|---|

| Scale commodities | Large cement, steel, base materials groups | High-volume, standardized output | National to multi-region distribution; logistics-heavy networks | Cycle-driven; competitive on delivered cost | Lowest delivered cost, scale reliability, channel coverage | Pricing compresses in down-cycles; slower differentiation |

| Tier-1 engineered manufacturing | Auto majors, top component suppliers | Engineered parts with repeatable quality (high-volume) | Deep OEM relationships; plant-adjacent supply chains; multi-plant footprints | Cost-plus / negotiated; tightly benchmarked by OEMs | Quality systems, vendor approvals, supply assurance, process capability | Program concentration risk; painful spec changes; penalties for line stoppage |

| High-compliance specialists | Aerospace/defense suppliers, precision shops | Low-volume, high-spec components; qualified part numbers | Niche global reach via certifications and approvals; fewer but deeper accounts | Premium pricing justified by qualification and risk reduction | Certification moat, traceability, documentation discipline, switching costs | Long sales cycles; high qualification CAC; working-capital strain |

| Electronics manufacturing services (EMS) | EMS leaders, component ecosystem | Build-to-print sub-assemblies and final assembly; fast ramps | Global OEM programs; cluster-driven ecosystems; multi-site scale | Competitive; margin tight, pricing tied to yield and volume | Speed, yield, procurement efficiency, program execution | Customer concentration; rapid scale magnifies quality failures; WC intensity |

| Platforms and orchestrators | Manufacturing platforms | Aggregated capacity + supplier management + fulfillment orchestration | Broad reach through supplier networks; flexible cross-region sourcing | Value-based (time saved / risk reduced); can undercut on speed | Fast sourcing cycles, flexible capacity, centralized project management | Quality variance if governance is weak; supplier dependency risk |

SWOT-Style Summary of Top 5 Players

| Company / Segment | Strengths | Weaknesses | Opportunities | Threats |

|---|---|---|---|---|

| Maruti Suzuki (Passenger Vehicles) | Dominant domestic market share; strong distribution network; scale-driven cost efficiency | Heavy exposure to mass-market segments; margin pressure in competitive categories | Export growth; EV portfolio expansion; operational efficiency improvements | SUV-heavy competition; EV transition risks; demand cyclicality |

| Tata Motors (Commercial Vehicles + PV presence) | CV market leadership; diversified product portfolio; strong domestic presence | Exposure to fleet demand cycles; margin variability | CV upcycle; infrastructure spending tailwinds; electrification | Competitive pricing pressure; input cost volatility; economic slowdown impact |

| UltraTech Cement (Cement Leader) | Scale advantage; strong regional presence; acquisition-driven growth; logistics network | Energy and fuel cost sensitivity; high capital intensity | Industry consolidation; infrastructure demand; pricing power in concentrated regions | Regional fragmentation; input cost spikes; regulatory tightening |

| Large Integrated Steel Producer (e.g., Tata Steel / JSW Steel archetype) | Captive raw materials; integrated operations; export capability | Highly cyclical pricing exposure; capital-intensive | Infrastructure demand; value-added steel products; downstream integration | Global oversupply; trade barriers; raw material price volatility |

| Dixon Technologies (EMS Leader archetype) | Rapid capacity scaling; OEM partnerships; category diversification | Customer concentration risk; working capital intensity | Expansion into IT hardware and industrial electronics; localization trend | Margin compression; quality failures at scale; global demand swings |

6. Trend Analysis & Forward Outlook

This is the part where the story stops being “manufacturing is growing” and becomes “manufacturing is being stress-tested.” Not by one thing, but by a stack: rates, trade uncertainty, compliance expectations, tech disruption, and the simple reality that global buyers have more options than they did a decade ago.Macroeconomic factors that will shape manufacturing (next 12–24 months)

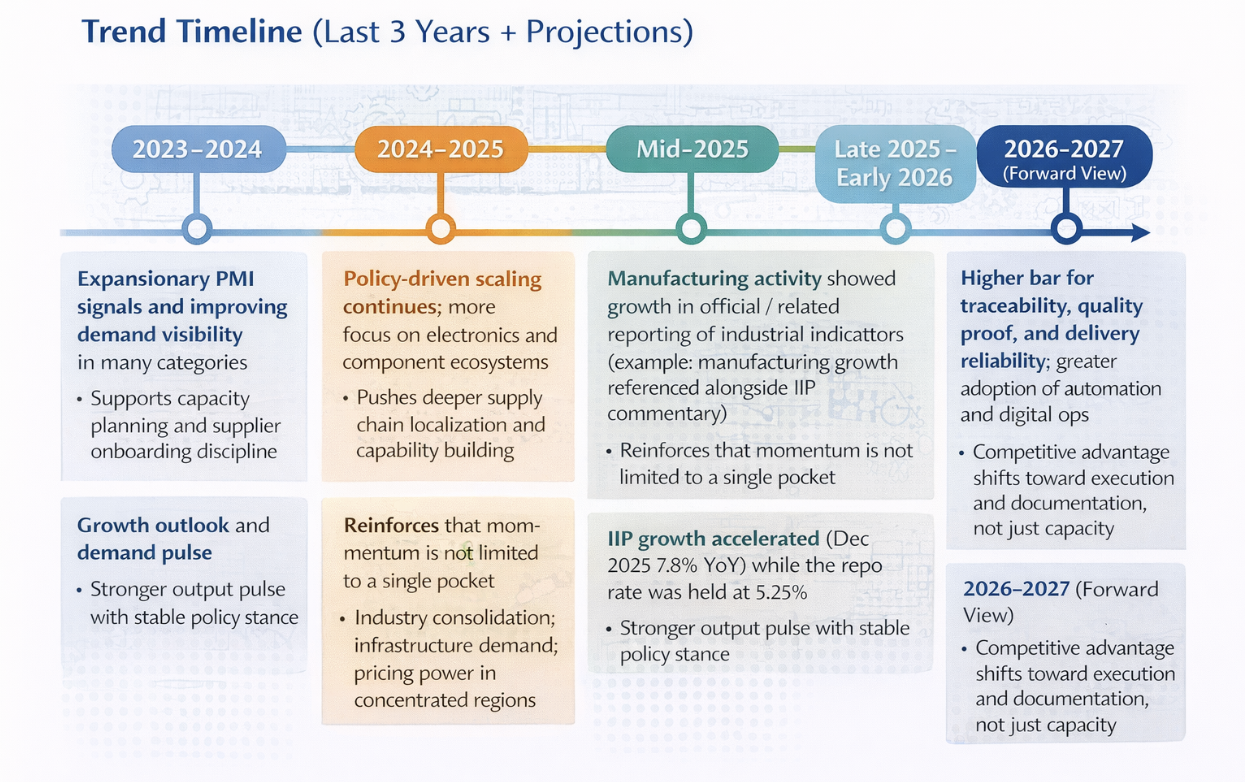

Interest rates and cost of capital India’s monetary policy stance matters because manufacturing is working-capital hungry and capex-heavy. In early February 2026, reporting indicates the RBI kept the repo rate unchanged at 5.25%. (The Times of India, Goodreturns) Implication for manufacturers: • Expansion stays possible, but CFOs will keep demanding cleaner payback math. • Working capital discipline becomes a competitive advantage, not a finance hygiene task. Growth outlook and demand pulse On the demand side, near-term indicators look constructive: • RBI-reported/covered projections have FY26 real GDP growth around 7.4% (as reported in multiple outlets). (The Economic Times, The Economic Times) • IMF country data shows India’s 2026 projected real GDP growth at 6.4% (WEO update referenced on IMF’s India page). (IMF) • Industrial output (IIP) growth was reported at 7.8% YoY in Dec 2025, the highest in over two years per Business Standard’s reporting of MoSPI data. (Business Standard) What to take from that mix: The base case is still expansionary, but executives should plan for unevenness by subsector (consumer-facing categories can swing faster than infra-linked ones). Trade, geopolitics, and supply chain risk Even when domestic demand is strong, export-heavy manufacturers will be exposed to: • Trade policy uncertainty and compliance requirements from major markets • Logistics shocks (port delays, container pricing, lane disruption) The winners will be the firms that build redundancy and documentation systems early, because global buyers increasingly reward low-risk suppliers.Tech disruptions: AI, automation, and the new “minimum bar”

The next phase of Indian manufacturing competitiveness won’t be won on cheap labor alone. It’ll be won on repeatability, speed, and proof. Automation is moving from “nice-to-have” to “how you hit delivery promises” A visible signal: automation players are actively pushing more advanced systems into Indian operations, including robotics showcases at major industry events like LogiMAT India 2026. Practical impact you’ll see on factory floors: • More vision inspection for quality consistency • More predictive maintenance (even lightweight versions) to reduce unplanned downtime • More digital traceability demanded by export customers A useful mental model: If your competitor can quote faster, produce with fewer defects, and ship with tighter documentation, they don’t just win one PO. They get preferred-supplier status, which is where the real compounding happens.Consumer sentiment and downstream demand signals

Manufacturing doesn’t live in a vacuum. When rural demand or infrastructure spending accelerates, it hits upstream suppliers quickly. Example demand pulse: India’s tractor market reportedly started 2026 strong, with domestic sales up 43% YoY in January (reported in early Feb 2026). (The Times of India) This matters because tractors are a broad ecosystem signal: • Steel and castings • Hydraulics and precision components • Tires and rubber • Electronics and harnessesPredicted strategic moves by function (finance, marketing, ops)

These aren’t “bets.” They’re the moves you should expect rational operators to make if the macro stays broadly expansionary and compliance pressure keeps rising.Finance trends

- Capability acquisitions continue Expect more deals that buy certifications, customer qualifications, or advanced processes rather than pure capacity.

- Working capital becomes a board-level lever The simplest way to fund growth without stretching the balance sheet is to shorten the cash cycle. That’s not glamorous, but it’s powerful.

Marketing trends

- Proof-led positioning replaces brand fluff B2B buyers increasingly prefer rep-free research. That pushes marketing to become a “trust engine” with documentation, case evidence, and clear capability pages.

- More spend shifts to account-based plays for high-value segments For aerospace/defense/precision: fewer accounts, deeper persuasion, more qualification assets.

Operations trends

- Lane-level logistics optimization becomes standard Now that logistics cost is measured more rigorously, companies will optimize by corridor, mode, and port process rather than treating freight as a flat overhead.

- Quality systems and traceability become sales assets The plant that can demonstrate repeatability and traceability faster will win more export business.

Trend Timeline (Last 3 Years + Projections)

Forecasted Spend per Channel/Function

| Function | Spend direction (next 12–24 months) | What it shifts toward | Why |

|---|---|---|---|

| Finance | Slight increase | Selective M&A and capex with tighter ROI thresholds | Stable policy stance keeps growth feasible, but payback scrutiny stays high in capex-heavy businesses |

| Marketing | Moderate increase | Proof assets (qualification kits, case evidence), ABM for high-value accounts, digital self-serve research | Buyers research more before engaging sellers, and procurement teams reward audit-ready transparency |

| Operations | Highest increase | Automation, quality systems, traceability, lane-level logistics optimization | Execution and compliance increasingly define export readiness; reliability and documentation become differentiators |

7. Strategic Recommendations

The strongest manufacturing strategies in India right now share a common theme: reduce buyer risk while improving cash and execution. That sounds obvious until you watch how many firms chase growth without fixing the basics that make growth sustainable. Below is a set of recommendations you can hand to real teams. Each one links finance, marketing, and operations so it doesn’t collapse in implementation.Strategy Playbook Grid

| Function | Recommendation | What to do next (concrete actions) | Example impact |

|---|---|---|---|

| Finance | Make working capital a growth product | Set lane/SKU-level inventory targets; tighten credit terms by risk tier; reduce quote-to-invoice cycle time; run a weekly cash war-room for top 20 customers | Frees cash to fund capex and hiring without stretching debt |

| Finance | Use capability-led M&A or partnerships, not “capacity for capacity’s sake” | Target acquisitions/partners that bring certifications, advanced processes, or customer approvals; integrate quality systems first | Speeds entry into higher-margin segments; reduces time-to-qualification |

| Finance | Build a “profitability truth” view by customer and lane | Allocate freight, rework, and warranty costs to customers/SKUs; flag negative-contribution accounts; renegotiate commercial terms using data | Stops silent margin leaks; improves pricing discipline |

| Marketing | Turn compliance into your best-performing asset | Publish a qualification kit landing page (certs, process flow, inspection steps, sample docs); create buyer-ready proof packs by segment | Higher shortlist rate; fewer procurement objections; faster audits |

| Marketing | Shift from broad awareness to account-based trust building (ABM-lite) | Identify 30–100 high-value target accounts; build content per persona (procurement vs engineering); run sequences that link to proof assets | Lowers wasted spend; improves meeting quality and pipeline conversion |

| Marketing | Make “speed of quoting” part of the brand | Launch a 48-hour RFQ pledge with a clear input checklist; track SLA performance internally; build a quoting playbook | More RFQs convert to orders; less sales churn and back-and-forth |

| Operations | Treat OTIF as a commercial metric, not a factory metric | Track OTIF by customer tier and lane; add root-cause tagging (planning, vendor, QA, logistics); review weekly with sales + ops together | Higher retention; fewer penalties; stronger preferred-supplier positioning |

| Operations | Invest in traceability and documentation before you’re forced | Standardize inspection reports and CoA templates; implement lot-level traceability for export customers; train supervisors on documentation discipline | Faster audits; reduced rejection risk; stronger export credibility |

| Operations | Reduce “time tax” in logistics through lane optimization | Build a lane profitability map; renegotiate by lane (not vendor); reduce documentation delays with a checklist; shift mode mix where feasible | Lower delivered cost; fewer missed vessel cutoffs; tighter lead times |

| Operations | Automate where it hits quality and downtime first | Prioritize vision inspection for critical defects; basic predictive maintenance for top failure assets; digitize downtime and scrap reporting | Better yield stability; less rework; more predictable output |

| Cross-functional | Build one shared scorecard across teams | Single weekly dashboard: RFQs, quote SLA, OTIF, defect rate, inventory days, cash conversion cycle; assign owners | Eliminates silo behavior; makes performance visible and improvable |

8. Appendices & Sources

This section consolidates the structured data used across the report, provides citation transparency, and outlines limitations. The goal is clarity, not volume.Raw Data Tables

Industry Snapshot Data

| Metric | Value | Unit | Source |

|---|---|---|---|

| Manufacturing GVA (FY24) | 24.6 | INR lakh crore | Economic Times (official data reference) |

| Manufacturing GVA Growth (FY24) | 11.9 | % YoY | Economic Times (official data reference) |

| Logistics Cost (FY24) | 7.97 | % of GDP | DPIIT/NCAER Logistics Cost Study |

| Total Logistics Cost (FY24) | 24.01 | INR lakh crore | DPIIT/NCAER Logistics Cost Study |

| PLI Reported Investment (through Nov 2024) | 1.61 | INR lakh crore | Press Information Bureau |

| PLI Production/Sales (through Nov 2024) | 14 | INR lakh crore | Press Information Bureau |

| PLI Employment (direct + indirect) | 11.5 | lakh jobs | Press Information Bureau |

Select M&A Transactions Referenced

| Buyer | Target | Segment | Deal Value (INR crore) | Announcement Year | Source |

|---|---|---|---|---|---|

| JSW Paints | AkzoNobel India (stake up to 74.76%) | Paints & Coatings | 8986 | 2025 | Business Standard |

| Tata Electronics | Pegatron Technology India (60% stake) | Electronics Manufacturing Services | Undisclosed | 2025 | Tata Electronics Press Release |

| Tube Investments of India | Orange Koi (87% staged acquisition) | Precision Manufacturing | 73 | 2026 | Times of India |

| Sigma Advanced Systems | AS Strategic | Aerospace & Defense | 30 | 2026 | Economic Times |

Illustrative Valuation Multiples (Directional Ranges)

| Subsector | EV / Revenue (Low) | EV / Revenue (High) | EV / EBITDA (Low) | EV / EBITDA (High) |

|---|---|---|---|---|

| Steel & Base Metals | 0.8 | 1.8 | 5 | 9 |

| Cement | 2.0 | 4.0 | 10 | 18 |

| Specialty Chemicals | 2.5 | 6.0 | 12 | 25 |

| Auto Components | 1.5 | 3.5 | 8 | 16 |

| Electronics Manufacturing Services (EMS) | 1.0 | 3.0 | 10 | 20 |

| Aerospace & Defense | 2.5 | 6.0 | 15 | 30 |

| Industrial Automation & Capital Goods | 1.5 | 4.0 | 12 | 22 |

Hyperlinked Source List

Macroeconomic & Industry Data Manufacturing GVA FY24 and growth https://economictimes.indiatimes.com/news/economy/indicators/manufacturing-gva-rises-12-in-fy24-employment-up-6/articleshow/123551232.cms India Manufacturing PMI (HSBC reporting) https://www.moneycontrol.com/economic-calendar/india-s%26p-global-manufacturing-pmi/1414724 MSME contribution to output and exports (Economic Survey reporting) https://m.economictimes.com/small-biz/sme-sector/msme-sectors-role-critical-in-enabling-effective-supply-chain-participation-eco-survey-2025-26/articleshow/127765473.cms PLI Investment and Production Data https://pib.gov.in/PressReleasePage.aspx?PRID=2114011 FDI Manufacturing Inflows https://pib.gov.in/PressReleasePage.aspx?PRID=2086347 Logistics Cost Assessment (DPIIT/NCAER) https://www.dpiit.gov.in/static/uploads/2025/09/7d467e0f4aee2362e4bf90b84b7a5332.pdf Industrial Production (IIP reference) https://www.business-standard.com/economy/news/iip-december-2025-industrial-production-output-manufacturing-construction-126012800955_1.html Market Share Data (Automotive Retail FY’25) https://www.fada.in/images/press-release/167f3463b1a212FADA%20Releases%20FY%202025%20and%20March%202025%20Vehicle%20Retail%20Data.pdf Steel Production Data https://steel.gov.in/sites/default/files/2025-04/Annual%20Report%202023-24%20Final_0.pdf Select Deal References JSW Paints – AkzoNobel India https://www.business-standard.com/companies/news/jsw-paints-to-buy-akzo-nobel-india-in-1-08-billion-deal-to-boost-market-share-125062700199_1.html Tata Electronics – Pegatron https://www.tataelectronics.com/w/tata-electronics-announces-acquisition-of-majority-stake-in-pegatron-technology-india Tube Investments – Orange Koi https://timesofindia.indiatimes.com/city/chennai/tii-to-buy-orange-koi-enter-metal-injection-molding-biz/articleshow/127998126.cms Sigma Advanced Systems – AS Strategic https://m.economictimes.com/news/defence/hyderabads-sigma-advanced-systems-buys-as-strategic-to-expand-global-aerospace-defence-platform/articleshow/128200801.cmsMethodology Notes

Data Selection Where possible, primary government releases (PIB, DPIIT, Ministry reports) were used. Market-share and deal references rely on reported industry coverage. Valuation Ranges EV/Revenue and EV/EBITDA multiples are directional ranges derived from public market observations across comparable listed firms. Exact multiples fluctuate based on:- Business cycle position • Leverage levels • Growth expectations • Commodity price environment • Export exposure

Data Limitations

- Indian manufacturing is highly heterogeneous; aggregate figures may mask subsector volatility. • M&A deal values are sometimes undisclosed; reported values may reflect stake purchases rather than full enterprise values. • PMI and IIP are macro indicators; they do not evenly represent all manufacturing categories. • Valuation multiples shift rapidly with global liquidity and commodity cycles. • MSME data is often survey-based and may have reporting lags.